Does Your Product Have a Lifespan?: Managing Product Life Cycle (PLC)

The theory of Product Life Cycle (PLC) states that every product has a life cycle, starting with an introduction, development, growth, maturity, and decline. This blog explores what each stage of PLC entails and inventory management tips for each stage of product life.

Every product has a life cycle, starting with its introduction to the market, growing slowly, gaining popularity, reaching maturity, and eventually disappearing. This theory, known as the Product Life Cycle (PLC), is analogous to a person's life. Understanding the PLC is crucial for various aspects of a business. Knowing the product's life cycle enables more rational inventory management. In this blog post, we will delve deeper into the product life cycle and explore its relevance to inventory management.

Product Life Cycle (PLC)

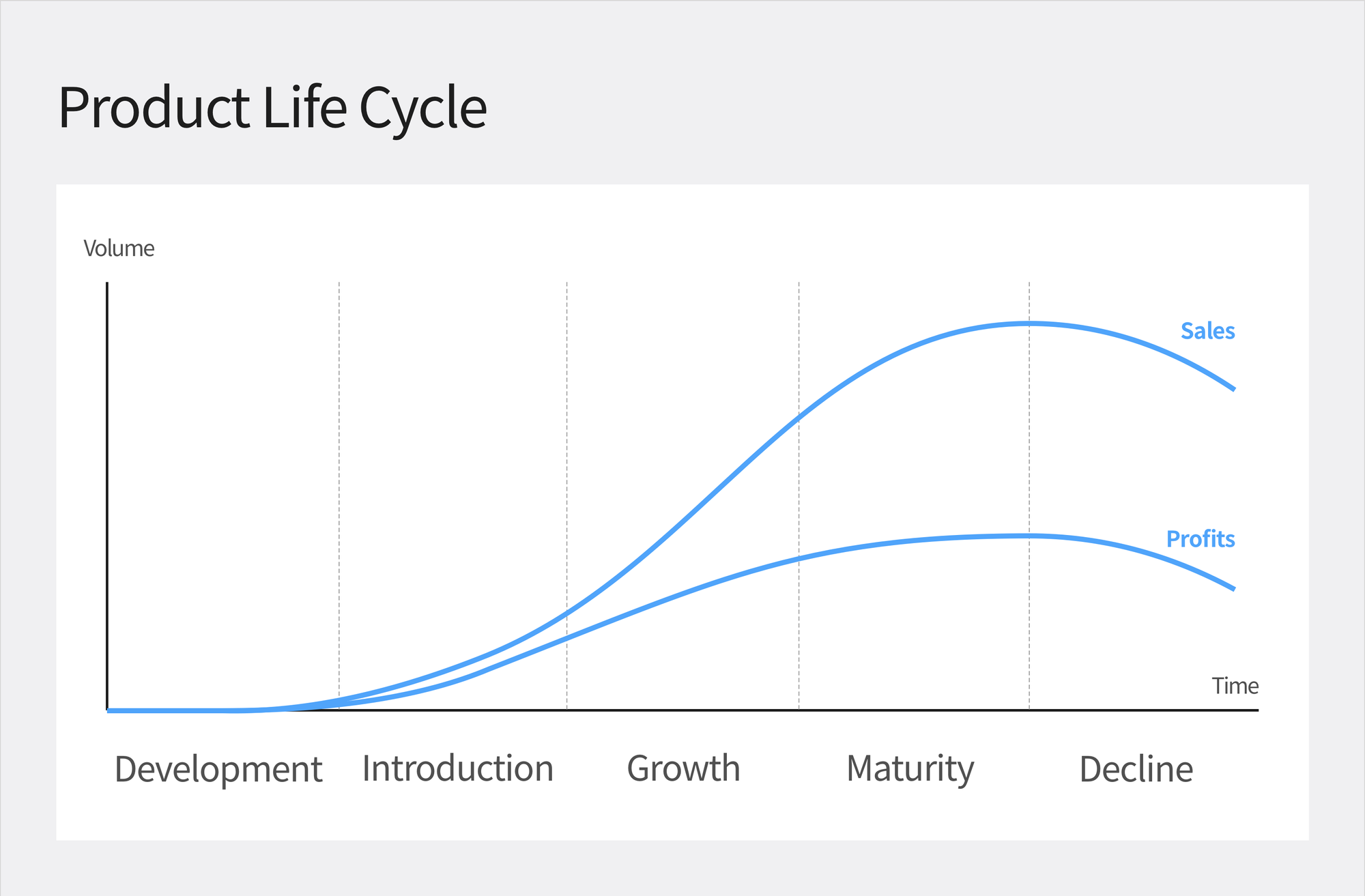

As mentioned above, the Product Life Cycle (PLC) is a theory that illustrates how a product's journey from ideation to discontinuation. It can be broken down into five stages: development, introduction, growth, maturity, and decline. For companies that produce products, understanding which stage of the PLC their product is in is crucial. This knowledge allows for better decision-making and enables appropriate inventory management based on the specific stage.

Stage 1: Market Development

The initial stage of the product life cycle referred to as the development stage, involves multiple steps before a new product can be introduced to the market. These steps involve idea generation, product concept decision-making, prototyping, and product launch strategy development. Despite possessing groundbreaking ideas, many early-stage companies fail to obtain the necessary funds for product development. The companies often showcase prototypes to manufacturers or investors to secure funding. Once the manufacturers or investors acknowledge the product's potential, they provide funding to proceed with manufacturing.

Stage 2: Market Introduction

Have you launched your product in the market? If so, you have entered the introduction phase, where you must actively promote and market your newly released product to increase its visibility to potential customers. The primary goal of this phase is to enhance product awareness by focusing on increasing its visibility while carefully monitoring the responses of potential customers.

Do not produce large quantities of products during the introduction phase when sales are still low. It is a shortcut to increase inventory levels. Avoid incurring high inventory maintenance costs by negotiating with the manufacturer to produce small quantities. However, be mindful of not driving up the unit cost due to a low minimum order quantity (MOQ). Click here to learn more about MOQ.

Stage 3: Market Growth

With the gradual increase in product awareness, sales have surged, indicating the onset of the growth stage. During this stage, the number of consumers actively seeking the product increases rapidly, leading to a natural expansion of the market and an increase in competitors. To gain a competitive edge, businesses must secure new distribution channels and provide more convenient customer support services.

Businesses must prioritize inventory management, due to the significant increase in product inventory movements resulting from the influx of customer demand at this stage. To prevent costs from inventory shortages, it is essential to adjust production strategies from small to large scale. Inventory stockout costs can lead to missed sales opportunities and lost profits.

Stage 4: Maturity

As a company progresses, it enters the mature stage where there is a steady revenue flow, even if sales do not increase rapidly. This stage allows for an increase in revenue without a continuous upward trend in sales. Stabilized mass production reduces preparation costs significantly. However, complacency can cause a business to lose customers to increasing competitors. Instead of being content with stable revenue, businesses should strive to differentiate themselves to attract more loyal customers. The ultimate goal of the mature stage is to attract more loyal customers.

Even in the mature stage, businesses should practice inventory management tailored to mass production, just like in the growth stage. Based on stabilized revenue data, businesses can develop strategies to reduce inventory by forecasting demand, or explore various inventory management systems that many companies apply. Click here to learn more about inventory management systems.

Stage 5: Market Decline

During the mature stage, neglecting to implement effective customer management or tarnishing the brand image can cause a decrease in competitiveness, leading the product to enter its decline stage. This stage presents a pivotal decision for businesses as sales gradually decrease. While a business may endeavor to innovate its product in a novel direction, it may also have to discontinue the product. Regardless of the chosen approach, even product innovation mandates revisiting the product life cycle stage from the start, making the end of the product's life cycle inescapable.

Failure to acknowledge a product's decline stage and persist in production can lead to substantial expenses in inventory management. Implementing sales strategies such as bundling products or incorporating them into new ones can help dispose of inventory when a product has reached its decline stage.

The product life cycle is influenced by market conditions and product type, but the fundamental truth that all products have a life cycle, similar to humans, remains unchanged. It is recommended to monitor sales trends objectively to determine which stage the product is in, and then implement appropriate inventory management for each stage. By developing inventory management strategies based on the inventory life cycle, businesses can reduce inventory costs and increase profits.